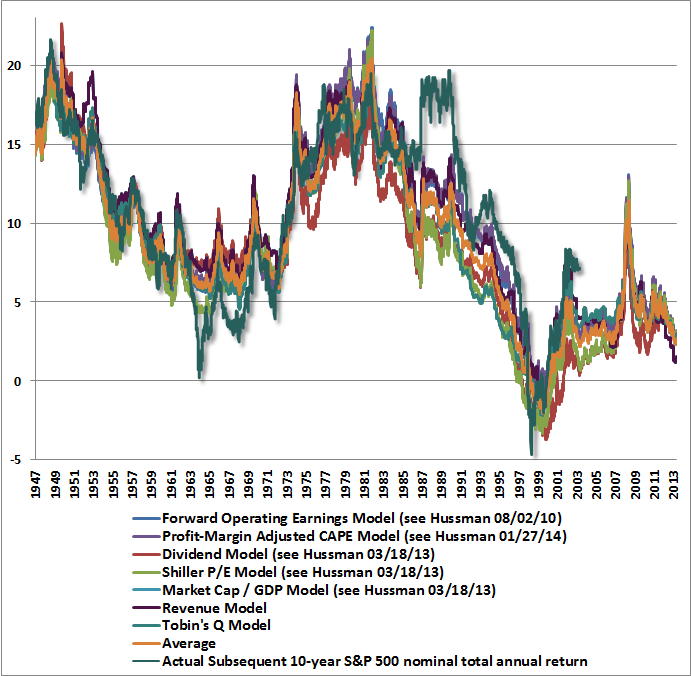

Based on forward p/e ratios the market is not overvalued. Yet, this is due to record margins and very low labor share. As a market historian said, profit margins are the most mean reverting historical data series we have. If they don’t revert, capitalism doesn’t work. Also valuation measures are not short term timing models. To wit: The irrational exuberance speech by Greenspan, Dec. 1996. If you look below you can see the models, at that time, were pointing to a fairly low expected future return, yet it took 6 years for markets to be reasonable again and it took over 10 years to be cheap again. I have spent a quite a bit of energy on this over many years. About all you can say, with a fair degree of confidence, is the total real return for stock prices over the next 7-10 years will be about -10%. Nobody knows how we get there.

US Large: -1.1% to -1.6%

US Small: -4.5% to -5.1%

US High Quality: 2.7% to 2.1%

Intl Large: 1.5% to 1.0%

Intl Small: 0.7% to -0.1%

Emerging: 4.2% to 4.1%